In her 2025 UK Budget statement, the chancellor, Rachel Reeves, reiterated the government’s pre-election pledge not to increase Income Tax, National Insurance contributions (NICs), or VAT.

However, she did announce an extension of the freeze on Income Tax thresholds.

This is likely to result in higher Income Tax bills, despite the actual headline tax rates remaining unchanged.

Discover why that’s the case and how it could affect you as an Australian expat living and working in the UK.

Also, read about steps to help you mitigate the effects of frozen thresholds.

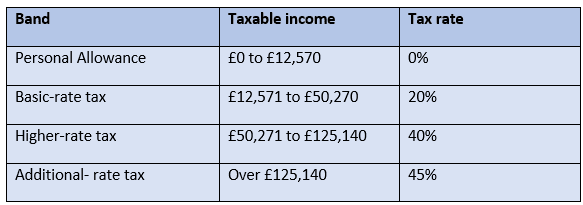

UK Income Tax thresholds will remain frozen until 2030/31

As in Australia, the amount of Income Tax on your earnings is driven by the levels at which different rates start to apply. These are known as “thresholds”.

The following table shows the Income Tax thresholds for 2025/26.

Before 2021, thresholds were usually increased in line with inflation. This meant you were not automatically pushed into a higher tax bracket as your income increased each year.

Since then, your Personal Allowance and Income Tax thresholds have been frozen by successive chancellors, and the hold has now been extended again until 2030/31.

This means that as your earnings increase, a larger proportion could be subject to a higher tax rate.

You may have seen this referred to as “fiscal drag”, and it can mean that the value and purchasing power of your earnings reduce over time.

Other taxes you may be liable for could be affected by the freeze

Fiscal drag also impacts other taxes you may be liable for. This is because the rate you pay for certain taxes is dependent on your marginal rate of Income Tax.

For example, if you are a basic-rate taxpayer, you will be liable for Capital Gains Tax at 18%, but if you are a higher- or additional-rate taxpayer, you’ll pay 24%.

This means that if thresholds remain unchanged and do not keep pace with inflation, you could end up being liable for significantly more tax on your capital gains than you were previously.

Additionally, your Personal Savings Allowance reduces from £1,000 to £500 if you are a higher-rate taxpayer, and is removed entirely for additional-rate taxpayers. This means you could pay tax on a larger portion of the interest you earn from cash savings.

Also, the rate at which you pay tax on your dividend income is dependent on your Income Tax marginal rate.

It can make sense to try to stay in a lower tax band

The overall effect of fiscal drag could significantly impact your personal finances. As a result, it could be prudent to take steps to reduce your taxable income and avoid moving into a higher tax band, if possible.

Three strategies you might want to consider are:

1. Pension contributions

If you are close to an Income Tax threshold, you may be able to reduce your taxable income and remain in the lower tax band by increasing your pension contributions.

Not only could this help you stay below an Income Tax threshold, but it will also boost your future retirement fund. It’s also highly tax-efficient, as you will benefit from tax relief at your marginal rate of Income Tax.

Furthermore, if your employer runs a salary sacrifice scheme, pension contributions are deducted from your gross salary before Income Tax and National Insurance (NI) are calculated. This potentially reduces the amount you pay.

Be aware that contributions under a salary sacrifice arrangement will be restricted from 2029, so it could be advantageous to maximise the opportunity to reduce your liability now if you are able to.

2. Claiming expenses

If you spend your own money on work-related expenses such as business mileage and equipment needed for your job, claiming tax relief can help reduce your Income Tax liability and potentially prevent you from moving into a higher tax band.

3. Making charitable donations

If your employer runs a “give as you earn” (GAYE) arrangement, you may be able to reduce your tax liability and support good causes through charitable donations.

GAYE donations are deducted from your monthly salary before Income Tax is calculated, and can help reduce your overall taxable income.

The freeze could affect you if you are drawing income from your Australian super

If you are an Australian expat who has already retired, frozen thresholds could have an effect on your retirement income planning.

You may be drawing a regular income from your Australian super which is subject to Income Tax in the UK

If that’s the case, you clearly need to be aware of how Income Tax thresholds can affect the amount of tax you could be liable for, and how a freeze in those thresholds will impact on you.

We would recommend that you get expert advice regarding your income strategy in these circumstances.

Get in touch

Frozen thresholds are likely to affect your tax liability and increase the amount of Income Tax you owe if you don’t take steps to mitigate the effect they may have on your finances.

If you’re an Australian expat in the UK, we can help you assess how this could affect you and adjust your long-term plans accordingly, particularly if you plan to return to Australia in the near future.

Please note

The value of your investment can go down as well as up, and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

This article is for informational purposes only and does not take into account your personal objectives, financial situation, or needs.

Please do not solely rely on anything you have read in this article, and ensure that you conduct your own research to ensure any actions you may take are suitable for your circumstances.

All contents are based on our understanding of HMRC, which is subject to change.