The value of the Australian dollar against UK sterling peaked at AUD $2.14 on 8 April 2025, which was the highest rate since October 2015. At the time of writing, it remains high at $2.07.

Bearing this in mind, you may have considered ways to take advantage of this, particularly if you have assets in the UK that you are looking to transition to Australia.

For example, you may have a substantial pension fund in the UK. Given the current exchange rate and the purchasing power you would acquire, it’s certainly worth considering transferring it if you are planning to spend your retirement years in Australia.

Furthermore, pending changes in UK pension and Inheritance Tax (IHT) regulations make it all the more important that you consider this option.

So, now could be the perfect time to explore the benefits associated with moving your UK pension across to an Australian arrangement.

Here are five good reasons why you may want to consider doing so.

1. You would benefit from a strong exchange rate

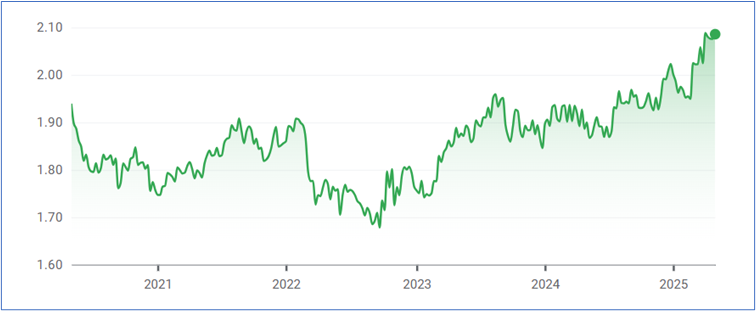

As you can see from the chart, the value of Australian dollars against the UK pound has increased by 24%, from a low point of $1.67 in September 2022 to a current rate of $2.07.

Source: Google.com

This can clearly be advantageous if you’re looking to transfer money from the UK to Australia. You’ll be buying far more Aussie dollars for your sterling than you would have done just a short time ago.

If you are thinking of transferring your accrued UK pension funds to an Australian super, this favourable exchange rate could be the prompt you need to take the next step in the transfer process.

Not only that, but you will also remove any future concerns about varying exchange rates throughout your retirement.

2. Transferring could help you avoid a substantial Inheritance Tax charge

From April 2027, UK pensions will be included in the value of your estate when it comes to assessing your liability for Inheritance Tax (IHT).

This means that even if you’re living in Australia, your pension fund could be taxed at 40% on your death, along with your other UK-based assets.

This impending change clearly raises issues around your legacy planning, and you will likely want to consider taking steps to reduce your liability.

By transferring your accrued UK pension to Australia, you may be able to avoid this potential tax charge, meaning that your beneficiaries could be better off when you pass away.

You should be aware that you have to be 55 before you can make such a transfer, rising to 57 in 2028. But even if you are not currently old enough, it’s important to get expert advice with regard to your UK estate planning.

3. You would create a highly advantageous tax scenario for yourself

In Australia, once you reach age 60 and have retired, all income and lump sums you draw from your super funds will generally be free from tax.

Conversely, income and lump sums taken from UK pension schemes will be taxed at your marginal rate of Income Tax, except for your 25% tax-free entitlement.

The key tax advantages for your UK pension occur when you’re making contributions to your fund, as tax relief at your marginal rate makes them a highly tax-efficient way to save for your retirement.

This means you can create a highly advantageous tax position for yourself if you transfer a pension to a super, with tax relief on your contributions and no tax on withdrawals.

So, transferring your UK pension to a super can provide you with significant tax savings during your retirement years.

4. Your retirement fund will be in the same country where you will be retiring

Although it is possible to manage most financial transactions online, it can make sound financial sense to have your retirement fund in the same country as where you will be spending your retirement.

Furthermore, if you are spending Australian dollars on a day-to-day basis, it makes sense to have your retirement fund in the same denomination.

By transferring your pension to an appropriate Australian super fund, you will be able to manage and access your funds locally, where you plan to spend your retirement.

As you have already read, this will also avoid any long-term currency risk, whereby the value of your fund could be seriously affected by any big fluctuation in the exchange rate between Australia and the UK.

5. It’s a great opportunity to consolidate all your pensions into a single fund

Another advantage of transferring your accrued UK pension fund to an Australian super is that it gives you the opportunity to combine all your retirement funds into a single arrangement.

One plan is far easier to control and manage than a series of them. This is especially the case when it comes to key issues such as your investment strategy, and when you start withdrawing income in retirement.

You may well have a series of UK pension funds that you have accumulated during your working life in the UK, along with super arrangements from previous Australian employer schemes, or through discretionary contributions you’ve made yourself.

By transferring to a new super fund, you will be able to transfer all your UK pensions to it, subject to eligibility. It will also be a good opportunity to consolidate any different super funds you may have into a single plan.

However, you should be aware that consolidation may not be the right thing for you to do, as you may miss out on valuable additional benefits related to your pension funds. Because of this, we would strongly recommend that you get expert advice before proceeding.

Find out more

Can I transfer my UK pension to Australia?

Why you could really benefit if you transfer your UK pension to Australia

Get in touch

Your ability to transfer your pension is subject to eligibility, and we would strongly recommend that you take expert financial advice before starting on the process.

Our guide – Transferring your UK pension to Australia – gives you more information about eligibility and the process involved.

If you’d like to learn more about transferring your pension and making the most of these advantages, we’re here to guide you through the process.

Get in touch to find out how we can help you.

Please note

The value of your investments can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

This article is for information only. Please do not solely rely on anything you have read in this article and ensure that you conduct your own research to ensure any actions you may take are suitable for your circumstances.

All contents are based on our understanding of HMRC and ATO legislation, which is subject to change.