Assessing risk is a fundamental part of managing your personal finances.

For example, investment risk is clearly a key consideration when you are putting together a portfolio to grow your wealth or build a pension fund.

However, if you’re an expat with assets in both the UK and Australia, one risk that is easy to overlook but which you need to take seriously is currency risk.

This is the possibility that fluctuations in foreign exchange rates could reduce the value of your wealth and affect various aspects of your cross-border financial planning, including your income, savings, and investments.

Read on to discover more about currency risk, how it can affect you, and how you can mitigate it.

Exchange rates are driven by a series of variable factors

For expats or those moving regularly between the UK and Australia, currency risk is a financial fact of life.

You may be living and working in the UK but still have assets and liabilities in Australia denominated in dollars. Similarly, you may be an Australian resident but have income from a property or an investment portfolio in the UK.

A range of factors determines exchange rates between the UK and Australia.

These could include the relative strength of the two economies, differing government policies, and broader geopolitical events over which neither country has any control.

When exchange rates move significantly, your financial plans can quickly become more expensive or less valuable.

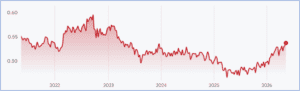

Two charts illustrate clearly how exchange rates can fluctuate.

1. AUD to GBP exchange rates

Source: Google

If you have bought UK sterling with Australian dollars over the last five years, the rate will have varied between 46p and 59p – a variation of over 20%.

2. GBP to AUD exchange rates

Source: Google

Likewise, the rate of return on your Australian dollar purchases made with sterling over the last five years has fluctuated between AUD$1.67 and AUD$2.08.

Transferring money between the UK and Australia

Currency risk becomes particularly important if you are an expat regularly transferring money between countries.

There are a range of reasons why you may do this, including:

- Making mortgage repayments in another country

- Investing in overseas holdings

- Making pension contributions, or drawing income from your fund

In all those examples, even relatively small exchange rate movements can have a major impact over time.

You don’t have to be transferring money to feel the impact

As well as moving money between countries, you also need to be aware of the potential currency risk related to assets you hold denominated in multiple currencies.

These could include pension and investment arrangements in both the UK and Australia.

If one currency is appreciably stronger than the other, it could result in the purchasing power of your money being reduced.

For example, if you are planning to retire in Australia with UK-based assets, you may be exposed to currency risk if sterling weakens against the Australian dollar, as it will take more pounds to buy the same amount of Australian currency.

This risk can feel more pronounced in retirement, when you’re relying on accumulated assets and have less scope to rebuild capital.

As a retiree, if you have assets in two financial jurisdictions, your future living expenses will depend on exchange rates at the time. A pension that feels substantial in one country may stretch far less in another if currency markets move against you.

3 ways you can mitigate currency risk

Clearly, you have no control over currency exchange markets, but there are proactive steps you can take to minimise your exposure.

1. Diversify your currency holdings

One straightforward way to avoid the worst effects of currency fluctuations is to not concentrate all your savings and investments in a single currency.

Holding assets in multiple currencies reduces your dependence on a single exchange rate, much like a diverse portfolio, which can help you avoid the worst effects of stock market upheaval.

This applies to all your liquid financial assets, including your pension funds, investments, and cash holdings.

You could also hold your emergency funds in different currencies to give you some financial flexibility if the value of one currency suddenly fluctuates.

2. Use a currency exchange specialist

As with many other finance-related issues, it’s always beneficial to get expert advice about managing your money.

In the case of currency risk, an exchange specialist can provide you with valuable insight into currency movements. They can also suggest strategies to protect your money against currency fluctuations and use certain instruments to help you get the best possible exchange rates.

If you are transferring a large amount of money – perhaps from the sale of a property – between the UK and Australia, the difference of just a few percentage points on the rate you get can make a real difference to your finances.

Likewise, if you are moving regular amounts, a currency exchange specialist can help you schedule these and access forward contracts to mitigate risk.

We work with several experienced exchange specialists and appreciate the valuable role they play in helping you manage your finances.

3. Review your pension and investment strategies

As with all aspects of your finances, it can be highly advantageous to plan ahead and have a clear action plan for managing your cross-border financial transactions.

For example, having a clear idea of where you plan to spend your retirement can be important for managing your currency transactions between Australia and the UK.

Underpinning this will be establishing the sources of your retirement income and ensuring that these are correctly denominated when you need to access them.

The same applies to long-term planning around other assets, such as your investment holdings and property.

In each case, being an expat with cross-border assets adds a layer of complexity to your plans, making expert advice pay dividends.

Seek specialist financial planning advice

Currency fluctuations are a normal part of global financial life, but if you’re an expat, they can easily hurt your finances if you don’t plan for them.

As with investing, it’s impossible to accurately predict how exchange markets will move. Instead, your priority should be to ensure you have a resilient financial plan and are well placed to mitigate currency risk.

If you have complex cross-border finances, it can be highly beneficial to get expert advice from financial professionals who appreciate the challenges of managing financial assets in different countries.

Get in touch

At bdhSterling, we specialise in helping clients navigate the complexities of international financial planning. We understand the threats posed by currency risk and can help you arrange your finances accordingly.

Whether you’re managing assets in multiple countries or planning a move abroad, our expert advisers can help you build a resilient, long-term financial strategy.

Get in touch to find out how we can help you.

Please note

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

This article is for information only; it does not take into account your personal objectives, financial situation, or needs. Please do not solely rely on anything you have read in this article and ensure that you conduct your own research to ensure any actions you may take are suitable for your circumstances. All contents are based on our understanding of HMRC and ATO legislation, which is subject to change.